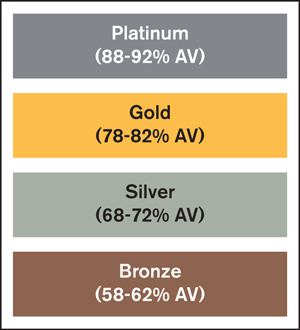

May 2013 – One of the objectives of the Affordable Care Act (ACA) is to standardize products in the individual and small employer markets through “Metal Levels.” Four metal levels will determine the type of health insurance that can be offered to individuals and small employers: Platinum, Gold, Silver and Bronze.

Additionally, the ACA outlines the percent of health care expenses that each metal level plan design would typically expect to pay for essential health care benefits. This is called the health plan’s “Actuarial Value.” For example, a health plan with a 70 percent actuarial value would on average pay 70 percent of expenses for essential health benefits with the enrollee paying 30 percent through a combination of co-pays, deductibles and co-insurance.

The four metal levels are defined by actuarial value targets that a qualified health plan must achieve, plus or minus 2 percent. For example, a silver plan must have an actuarial value of 68 percent to 72 percent.

In addition to the four metal level plans, “Catastrophic” plans are allowed in the individual health care market for young adults (under age 30).

Most health insurance insurers will offer benefits designs at all four of the metal levels. Insurers must offer at least one Silver and one Gold plan design if they are offering products on the federal or state marketplace (exchange).

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 17:00:002015-10-08 00:00:00Understanding Standardized Health Care Products Under the Affordable Care Act

May 2013 – Beginning January 1, 2014, individuals and employees of small businesses will have access to health care coverage through the Health Insurance Marketplace. Open enrollment of health insurance coverage through the Marketplace begins October 1, 2013. Under the ACA, employers must provide a notice of coverage options to each employee, regardless of plan enrollment status or part-time or full-time status. Employers are required to provide notice to existing employees no later than October 1, 2013, and new employees at the time of hiring beginning October 1, 2013.

The Department of Labor has developed model notice language which is available on the Department’s website: http://www.dol.gov/ebsa/healthreform/. There is one model notification for employers who do not offer a health plan and another for employers who offer a health plan to some or all employees. Employers may use one of these models, or a modified version provided that the notice meets the content requirements outlined in the model notifications.

The notice to employees must be provided in writing either electronically or via first-class mail.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 17:00:002015-10-08 00:00:00U.S. Department of Labor Provides Guidance on the Notice to Employees of Coverage Options under the Patient Protection and Affordable Care Act (ACA)

May 2013 – Nearly a year has passed since the Supreme Court upheld the Patient Protection and Affordable Care Act (PPACA). When President Obama was re-elected in November, reform became a certainty. Since that time, organizations, large and small, have struggled to understand the Act and how to comply.

A popular theme in discussions about health care reform has been cost. According to a recent Towers Watson report on health care benefits trends among employers, employers will spend an average of $9,248 per employee in 2013. It’s understandable to see why there’s so much trepidation among employers with 50 or more employees. Offering health care coverage can quickly add up to millions of dollars, cutting into profits. Quickly growing organizations on the verge of employing 50 FTEs must also prepare to comply with PPACA to avoid penalties.

An organization’s knee-jerk response to rising employee health care benefit costs might be to discontinue them altogether. This may be particularly attractive to organizations where the financial penalty for not offering coverage is significantly less than the cost to offer employee health care coverage.

Beware: focusing on the financial implications of health care reform alone can increase exposures to your organization in other ways. This is why it’s important to take a comprehensive, strategic approach to assessing health care reform and the implications for your organization.

Include Health Care Reform in Your Enterprise Risk Management Process

The decisions you make regarding health care reform will affect several areas of your organization. To properly assess the risk involved with your options, include health care reform in your enterprise risk management process.

Are You Prepared to Lose Talent?

An unintended consequence of discontinuing employee health care benefits could be loss of experienced talent. Organizations in industries that rely upon hard-to-find, highly skilled talent may put themselves at competitive disadvantage by choosing not to offer health care benefits or limiting employee hours to make certain individuals ineligible for benefits. Competitors could easily win the talent war by offering the highly valued benefits your company decided to do away with. In the short term, this move may save money, but in the long term, it could cost untold amounts in lost profits.

Do You Have an In-House Expert?

Health care reform is a complex issue. Most organizations don’t have an internal resource that fully understands all the implications. An independent advisor puts your best interest first. He or she can help you evaluate information from your insurance provider. In addition, an outside expert can help you devise a strategy to address the short-term and long-term increases and any other developments that arise along the way.

Health Care Costs are a HUGE Factor

Ultimately, businesses can’t escape the cost discussion. If your organization decides to continue offering health care benefits, there are cost-control methods you should consider:

Consider Self-Insuring

If your business is fully insured, you could consider self insurance. This generally means that your business would take on additional risk, but not all of it, for a reduction in premiums. If your business is currently self-insured, consider increasing your stop-loss point and reducing your premium.

Get the Best Price

Have you challenged your provider to give you the best price available? If not, this is the time to do it. Find out what your company can do to qualify for the discounts that are available.

Conduct a Claims Audit

Make sure your insurer is paying your claims accurately and that you are only paying for those eligible for benefits. You could be overpaying. An independent insurance consultant or an accounting firm with specialized services could assist you with this project.

Start a Captive Insurance Company

Captive insurance companies provide a formal method to reinsure, or to develop a fund to reduce your reliance on private insurance. This risk management tool has been used to reduce the cost of property & casualty insurance for many years. Rising health insurance costs make captive insurance companies a great option to help control those costs. Recent developments have made this captive option more accessible for smaller to mid-sized companies.

Form, or Join, a Private Exchange

Another potential solution is to form, or join, a private insurance exchange. This may be complementary to forming a captive insurance company, in that the entity forming it creates its own marketplace. This may qualify as providing insurance with a defined contribution that may help control costs and be compliant with PPACA regulations.

Ron Present is a principal in the Brown Smith Wallace health care industry services practice. He has more than a quarter-century of experience in the health care industry as an executive and consultant. He can be reached at 314.983.1358 or rpresent@bswllc.com.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 17:00:002015-10-08 00:00:00Big Picture: Don’t Lose Sight of it as You Focus on Health Care Costs

By Bonnie Bochniak

Vice President, Government Relations

MBPA/MFBA

May 2013 – The Michigan House of Representatives is taking on the issue of Medicaid Expansion, but on their own terms. Medicaid Expansion is an option for each state to adopt; it is not a requirement, per the Affordable Care Act (ACA). Currently 22 states, including Washington D.C., will have Medicaid Expansion and 14 states thus far have rejected the opportunity.

Medicaid Expansion would amend the Social Welfare Act to allow nondisabled adults with an annual income level up to 133% of federal poverty guidelines to enroll in the medical assistance program (Medicaid). Expanding this coverage would include about 450,000 working adults into Michigan’s Medicaid system. The cost savings to Michigan in accepting this expansion is about $1.5 billion in federal funds being received by the state in fiscal year 2013-2014 and an estimated $206 million in general fund due to the 100% federal payment of certain costs currently being financed with state funds.

Michigan House legislators are looking to propose their own spin on the Medicaid Expansion, calling for Medicaid Reform in House Bill 4714. Their changes to the federal guidelines cap those receiving federal assistance to 48 months, require 100% funding by the federal government, and requires that nondisabled adults enrolled in Medicaid make contributions of up to 5% of their annual income in the form of copays, premiums, or an account for health care expenses.

What this means for Michigan businesses is that some of their employees might qualify to receive health care through Medicaid, which depending on each company, can be very beneficial for the employer. The devil is in the details still, so much of this is currently being vetted out by legislators. This issue will see much more deliberation in the House and Senate.

We will continue to keep you up to date as more developments arise. As always, please contact our Government Relations team with any questions. By phone: 888-277-6464 or by email: bbochniak@michbusiness.org. We value your feedback.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 17:00:002015-10-08 00:00:00Medicaid Expansion in Michigan

May 2013 – The Departments of Labor, Health and Human Services and Treasury (“Agencies”) issued proposed regulations on the waiting period restrictions imposed by the Patient Protection and Affordable Care Act (PPACA). Under these provisions, effective with plan years beginning on and after January 1, 2014, employers are prohibited from imposing waiting periods applicable to their group health plans that exceed 90 calendar days.

For these purposes, a “waiting period” is the period of time that must pass before an eligible employee or dependent may enroll in the coverage under the group health plan. To be an “eligible” employee or dependent means that the individual has otherwise satisfied the eligible criteria under the terms of the group health plan (e.g., eligible job classification). Below are some of the key concepts employers should understand with regard to these provisions:

90 days means 90 days! The proposed regulations make it clear that the waiting period cannot exceed 90 days, and all calendar days are counted. Therefore, if the 91st day falls on a weekend or holiday, and due to administrative constraints the employee cannot be enrolled on that day, the employer must make coverage effective earlier than the 91st day. This also means that provisions such as “the first of the month following 90 days” will no longer be permissible.

The waiting period restrictions apply regardless of grandfathered plan status or employer size.

The provisions do not mandate a waiting period. Employers are not required to impose a waiting period for their group health plans, but rather if they elect to do so, it cannot exceed 90 calendar days.

The 90-day waiting period limitation does not apply to HIPAA-excepted benefits (e.g. standalone dental and vision plans, most health flexible spending accounts, fixed indemnity insurance, specified disease/illness policies, etc.).

Plan provisions that base eligibility on conditions other than the lapse of time are permissible so long as they are substantive and are not designed to avoid compliance with the 90-day waiting period restrictions (e.g., meeting certain sales goals, a specified level of commission, certain number of hours per period, etc.).

Cumulative hours of service requirements that do not exceed 1,200 hours are permissible, and the waiting period of no more than 90 days must begin once the new employee satisfies the cumulative hours of service requirement. However, employers should be cautious so as to not violate the employer shared responsibility provisions and open themselves up to potential penalties.

Currently there are no special exemptions or delayed effective dates for collectively bargained or multiemployer plans.

As always, it is important for employers to work closely with their legal counsel, benefits consultants, third party administrators and/or insurers to ensure compliance with PPACA. Employers should review their current group health plan waiting periods to ensure that it does not impose a waiting period of greater than 90 days after January 1, 2014 (or as of the start of the first plan year beginning after January 1, 2014 if the employer operates on a non-calendar year basis). Employers should also review, and amend where necessary, any group health plan documentation that details waiting periods such as plan documents, summary plan descriptions, underlying insurance certificates, employee handbooks, open enrollment materials, etc.

*This article is not intended to give legal advice. It is comprised of general information. Employers facing specific issues should seek the assistance of legal counsel.

Kristi R. Gauthier is a senior attorney in Clark Hill’s Birmingham office and concentrates her practice in Employee Benefits Law. Kristi has represented clients in a wide variety of employee benefits issues involving health and welfare benefits, as well as retirement plans. Kristi is admitted to practice in the State of Michigan, the U.S. District Court for the Eastern District of Michigan, and the U.S. Sixth Circuit Court of Appeals. She also is active in the legal community with memberships in the American Bar Association, the State Bar of Michigan, and the Oakland County Bar Association where she is a member of the Employee Benefits Committee. Kristi also serves as a member of the Clark Hill Diversity and Inclusion Committee. Kristi has lectured on various employee benefits issues, including ERISA compliance, healthcare reform, COBRA, section 125 plans, 403(b) plans and IRS plan correction programs. Kristi is also a co-author of the ABA publication ERISA Survey of Federal Circuits. Kristi was named a “Rising Star” by Michigan Super Lawyers in 2011.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 17:00:002015-10-08 00:00:00Agencies Shed Some Light on the Waiting Period Restrictions Under PPACA

In the January 30, 2013 BluesMarketplace, Blue Cross® Blue Shield® of Michigan and Blue Care Network (BCBSM and BCN) announced significant changes to the lead time requirements for 1-49 New Business groups.

A 21 calendar-day lead time is required for all New Business, except for those groups enrolling in a BCBSM Health Equity CDH plan, a BCN Healthy Blue LivingSM, HRA or HSA plan. These plans still require a 45 calendar-day lead time. The 21- or 45-day lead time is from when the managing agent receives the complete and accurate submission.

Important: Requests for short-lead times or retroactive exceptions will no longer be approved.

It is important to remember that lead time is calculated in calendar days, not business days.

Contact BCBSM or your Managing Agent for additional information and requirements that may be requested, as well as the life cycle of a New Business case, and a helpful document for building proper expectations with your clients.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 16:00:552015-10-08 00:00:00Agents…New BCBS Lead Time Requirements Reminder

Blues agents must complete sales training to meet accreditation requirements.

To sell our products in the ACA’s Health Insurance Marketplace, Blue Cross Blue Shield of Michigan must become accredited by the National Committee for Quality Assurance, also known as NCQA. Blue Care Network’s accreditation process is managed separately.

NCQA has outlined requirements that Blues agents must meet regarding outreach to prospective individual and group members — and to their employers, when applicable. The guidelines specifically address engagement prior to enrollment.

To ensure that we achieve accreditation, you must do the following:

1. Review individual and group sales training presentations:

2. Distribute The Value of Blues Coverage flier. The flier provides information we’re required by NCQA to tell prospective members. The above sales presentations detail how and when to distribute the fliers.

The fliers will also be posted in Agent Secured Services. The specific locations are listed in the attached presentations.

Questions? Contact your Blues sales representative or managing agent.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 16:00:502015-10-08 00:00:00Affordable Care Act Requires Blues Accreditation by National Committee for Quality Assurance

Beginning January 1, 2014, individuals and employees of small businesses will have access to health care coverage through the Health Insurance Marketplace. Open enrollment of health insurance coverage through the Marketplace begins October 1, 2013. Under the ACA, Employers must provide a notice of coverage options to each employee, regardless of plan enrollment status or part-time or full-time status. Your employer clients are required to provide notice to existing employees not later than October 1, 2013 and new employees at the time of hiring beginning October 1, 2013.

The Department of Labor has developed model notice language which is available on the Department’s website: http://www.dol.gov/ebsa/healthreform/. There is one model notification for employers who do not offer a health plan and another for employers who offer a health plan to some or all employees. Employers may use one of these models, or a modified version provided that the notice meets the content requirements outlined in the model notifications.

The notice to employees must be provided in writing either electronically or via first-class mail.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 16:00:452015-10-08 00:00:00U.S. Department of Labor Provides Guidance On The Notice To Employees of Coverage Options Under The Patient Protection and Affordable Care Act (ACA).

As a courtesy of the Michigan Business & Professional Association and the Michigan Food & Beverage Association, and working with our partner, Larry Grudzien, we’re pleased to offer you access to a FREE HSA Guide.

The guide explains every aspect of HSAs in fifty questions and answers format. It also includes the NEW 2014 contribution and coverage amounts and the required changes under health care reform.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2013-05-28 16:00:302015-10-08 00:00:00FREE HSA Guide for 2014 Now Available

The four metal levels are defined by actuarial value targets that a qualified health plan must achieve, plus or minus 2 percent. For example, a silver plan must have an actuarial value of 68 percent to 72 percent.

The four metal levels are defined by actuarial value targets that a qualified health plan must achieve, plus or minus 2 percent. For example, a silver plan must have an actuarial value of 68 percent to 72 percent. May 2013 – Beginning January 1, 2014, individuals and employees of small businesses will have access to health care coverage through the Health Insurance Marketplace. Open enrollment of health insurance coverage through the Marketplace begins October 1, 2013. Under the ACA, employers must provide a notice of coverage options to each employee, regardless of plan enrollment status or part-time or full-time status. Employers are required to provide notice to existing employees no later than October 1, 2013, and new employees at the time of hiring beginning October 1, 2013.

May 2013 – Beginning January 1, 2014, individuals and employees of small businesses will have access to health care coverage through the Health Insurance Marketplace. Open enrollment of health insurance coverage through the Marketplace begins October 1, 2013. Under the ACA, employers must provide a notice of coverage options to each employee, regardless of plan enrollment status or part-time or full-time status. Employers are required to provide notice to existing employees no later than October 1, 2013, and new employees at the time of hiring beginning October 1, 2013. By Ron Present

By Ron Present By Bonnie Bochniak

By Bonnie Bochniak By Kristi R. Gauthier, Esq.

By Kristi R. Gauthier, Esq.