Lorem ipsum dolor sit amet, consectetuer adipiscing elit. Aenean commodo ligula eget dolor. Aenean massa. Cum sociis natoque penatibus et magnis dis parturient montes, nascetur ridiculus mus. Donec quam felis, ultricies nec, pellentesque eu, pretium quis, sem.

Nulla consequat massa quis enim. Donec pede justo, fringilla vel, aliquet nec, vulputate eget, arcu. In enim justo, rhoncus ut, imperdiet a, venenatis vitae, justo. Nullam dictum felis eu pede mollis pretium. Integer tincidunt. Cras dapibus. Vivamus elementum semper nisi. Aenean vulputate eleifend tellus. Aenean leo ligula, porttitor eu, consequat vitae, eleifend ac, enim.

MBPA could help save you thousands of dollars in health care premiums and avoid possible penalties.

With Michigan’s expanded Medicaid program, you could have employees that may be eligible to enroll in the Healthy Michigan Plan, which could save an employer thousands of dollars annually in health care premiums.

If you are an “applicable large employer” who currently does not offer coverage to substantially all of its full-time employees, this would be a proactive way to assist your employees in obtaining health care coverage before the ACA employer shared responsibility penalties take effect. (Applicable large employers with 50-99 full-time equivalent employees (FTE) will be subject to the employer shared responsibility penalties beginning in 2016. Those with 100 or more FTEs will need to start offering health benefits to at least 70% of their FTEs by 2015 and 95% by 2016 in order to avoid potential penalties).

If just 5 employees qualify and choose to enroll in the Healthy Michigan Plan, the employer could potentially save a minimum of $21,000.00 a year!

Although an employer cannot force or coerce employees to enroll in the Healthy Michigan Plan, by simply educating the employees on the Healthy Michigan Plan including potential cost savings to them and possibly better health coverage including lower co-pays and out of pocket expenses than their current group plan, why wouldn’t an employee choose it?

Who Could Qualify for the Healthy Michigan Plan? Individuals who…

• Are age 19-64 years

• Have income at or below 133% of the federal poverty level* ($16,000 for a single person or $33,000 for a family of four)

• Do not qualify for or are not enrolled in Medicare

• Do not qualify for or are not enrolled in other Medicaid programs

• Are not pregnant at the time of application

• Are residents of the State of Michigan

* Eligibility for the Healthy Michigan Plan is determined through the Modified Adjusted Gross Income methodology.

How can MBPA help?

MBPA’s On-Site Enrollment Team will meet individually with employees that may qualify and further evaluate eligibility requirements for the Healthy Michigan Plan. If the employee is found to be eligible and wishes to enroll in the Healthy Michigan Plan, our team will then process their application and provide the employee with any on-going enrollment assistance that may be needed. Also, we would be happy to discuss our onsite service program with your trusted health insurance advisor to ensure they fully understand how this service may benefit you and your employees.

For more information on this new program, contact Jennifer Werner (ext. 166) at 888.277.6464

On July 24, 2014, the IRS released Revenue Procedure 2014-37 to index the Affordable Care Act’s (ACA) affordability percentages for 2015 under the employer mandate. The IRS also adjusted upward the income level under which employees are exempt from the ACA’s individual mandate.

Employer Mandate Adjustment

An applicable large employer’s health coverage will be considered affordable for plan Years beginning in 2015 under employer mandate if the employee’s required contribution to the plan does not exceed 9.56 percent of the employee’s household income for the year, up from 9.5 percent. This increase also applies to the three safe harbors that the IRS created in the regulations.

The reason for the increase is that the employer mandate was originally meant to take effect in 2014 but was subsequently delayed until 2015 or 2016, depending on employer size.

Individual Mandate Adjustment

Revenue Procedure 2014-37 also adjusts the affordability percentage for the exemption from the individual mandate for individuals who lack access to affordable minimum essential coverage. For plan years beginning in 2015, coverage is unaffordable for purposes of the individual mandate if it exceeds 8.05% of household income (as opposed to 8% originally).

This change stems from the requirement that the IRS must adjust the affordability percentage to reflect the excess of the rate of premium growth over the rate of income growth for the preceding calendar year, with each subsequent plan year being adjust accordingly.

For a copy of Revenue Procedure 2014-37, please click on the link below:

http://www.irs.gov/pub/irs-drop/rp-14-37.pdf

If you have any comments or questions regarding any of the above information, please do not hesitate to call me at (708) 717-9638 or e-mail me at larry@larrygrudzien.com

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2014-08-22 16:00:452015-10-08 00:00:00IRS Increases ACA’s Affordability Percentages for 2015

Question: My client with 75 full-time employees terminated their group health plan in 2014. When would they be subject to the employer mandate penalty? How is penalty determined?

When the employer mandate applies:

Answer: January 1, 2015

The penalty tax applies to “applicable large employers.” An applicable large employer is an employer who employed an average of at least 50 “full-time employees” on business days during the preceding calendar year, as provided in Code Section 4980H(c)(2)(A).

For 2015, the final regulations provide an important new transition relief for employers with less than 100 employees. If the following conditions are met, no penalty tax will apply until 2016 for employers with 50 to 99 employees:

* Limited Workforce Size. The employer employs on average at least 50 full-time employees (including full-time equivalent employees) but fewer than 100 full-time employees (including full-time equivalent employees) on business days during 2014. For this purpose, the determination of the number of full-time employees (including full-time equivalent employee) is made in accordance with the otherwise applicable rules for determining status as an applicable large employer.

* Maintenance of Workforce and Aggregate Hours of Service. During the period beginning on February 9, 2014, and ending on December 31, 2014, the employer does not reduce the size of its workforce or the overall hours of service of its employees in order to satisfy the workforce size condition set forth above. A reduction in workforce size or overall hours of service for bona fide business reasons will not be considered to have been made in order to satisfy the workforce size condition.

* Maintenance of Previously Offered Health Coverage. Except as otherwise provided in this subsection, during the coverage maintenance period the employer does not eliminate or materially reduce the health coverage, if any, it offered as of February 9, 2014. For purposes of this section, in no event will an employer be treated as eliminating or materially reducing health coverage if:

** it continues to offer each employee who is eligible for coverage during the coverage maintenance period an employer contribution toward the cost of employee-only coverage that either (A) is at least 95 percent of the dollar amount of the contribution toward such coverage that the employer was offering on February 9, 2014, or (B) is the same (or a higher) percentage of the cost of coverage that the employer was offering to contribute toward coverage on February 9, 2014;

** in the event there is a change in benefits under the employee-only coverage offered, that coverage provides minimum value after the change; and

**the employer does not alter the terms of its group health plans to narrow or reduce the class or classes of employees (or the employees’ dependents) to whom coverage under those plans was offered on February 9, 2014. For purposes of this requirement, the term coverage maintenance period means (1) for an employer with a calendar year plan, the period beginning on February 9, 2014, and ending on December 31, 2015, and (2) for an employer with a non-calendar year plan, the period beginning on February 9, 2014, and ending on the last day of the plan year that begins in 2015.

* Certification of Eligibility for Transition Relief. The applicable large employer certifies on a prescribed form filed with the IRS that it meets the eligibility requirements set forth above.

Since the employer terminated its plan in 2014, it is not eligible for the special transitional rule and will be subject to the employer mandate penalty on January 1, 2015.

Determination of the Employer Mandate Penalty Amount:

Generally, the employer mandate penalty under Code Section 4980H(a) is equal to the number of all full-time employees (excluding 30 full-time employees) multiplied by 1/12 of $2,000 for each calendar month.

Since the employer terminated its plan in 2014, it is also not eligible to use a transitional rule that increased the 30 employee reduction to 80 employees.

For 2015, the employer would be subject to a penalty of 75 -30 = 45 X $2,000 or $90,000.

For More Information: If you have any comments or questions regarding any of the above information, please do not hesitate to call me at (708) 717-9638 or e-mail me at larry@larrygrudzien.com.

In a recent newsletter that goes out to exchange navigators and certified application counselors only, officials at the Centers for Medicare & Medicaid Services (CMS) discuss the rules that govern exchange assisters’ activities.

These rules apply directly to those assisters for the Affordable Care Act (ACA) exchanges run by the U.S. Department of Health and Human Services (HHS), the parent of CMS. Some rules may also impact those assisters in state-based exchanges.

As a fresher, a certified Navigator (in-person assisters) provide unbiased information, at no cost, to help customers decide which health insurance option is best for them. Under the ACA, Navigators cannot recommend a specific plan to consumers.

HHS exchange assisters are not allowed to solicit door-to-door per sae. The consumer must initiate or ask the assister to come into their home. Once these terms are met, the in-person assister can sell exchange plans and services door-to-door, as long as they use a low-key approach.

More specifically, in an unsolicited visit, an assister can go door-to-door to educate consumers about the exchange system and the exchange application process. Then, and only then, after the initial conversation with the consumer educating them about the exchange, if initiated by the consumer, the assister may at that time help with enrollment, the application process etc.

As more information becomes public we will continue to keep you up to date as this unfolds. As always, we welcome your feedback and/or questions. Please feel free to contact our government relations staff at BBochniak@michbusiness.org

Note: The CMS exchange helper newsletter is not readily available to the public.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2014-08-22 16:00:352015-10-08 00:00:00HHS In-Person Assisters May Sell Door to Door

One of the fundamental flaws of the Affordable Care Act is that, despite its name, it makes health insurance more expensive. Today, the Manhattan Institute released the most comprehensive analysis yet conducted of premiums under Obamacare for people who shop for coverage on their own. Here’s what we learned. In the average state, Obamacare will increase underlying premiums by 41 percent. As we have long expected, the steepest hikes will be imposed on the healthy, the young, and the male. And Obamacare’s taxpayer-funded subsidies will primarily benefit those nearing retirement—people who, unlike the young, have had their whole lives to save for their health-care needs.

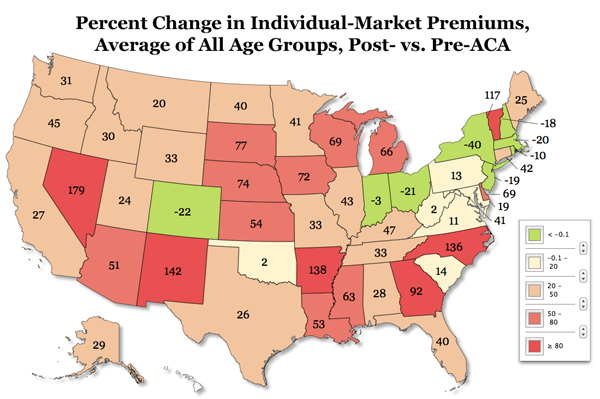

41 states, plus D.C., will experience premium hikes

If you’ve been following this space, you know that I and two of my Manhattan Institute colleagues—Yevgeniy Feyman and Paul Howard—have developed an interactive map where you can see how Obamacare affects premiums in your state. (If you ever need to find it, simply Google “Obamacare cost map.”)

In September, we released the first iteration of the map, which included data from 13 states and the District of Columbia. We only had data from a few mostly-blue states because the remainder were mostly participating in the federal exchange, and the federal exchange—for reasons we now understand more fully—hadn’t released any premium information at that time. That analysis found that underlying premiums would increase by 24 percent in those 13 states plus D.C.

Obamacare’s supporters argue that these rate increases aren’t important, because many people will be protected from them by federal subsidies. Those subsidies aren’t free—they’re paid for by taxpayers–and so it is irresponsible for people to argue that subsidies somehow make irrelevant the underlying cost of health insurance. Nonetheless, it’s important to understand the impact of subsidies on Obamacare’s exchanges; later in September, we released a second iteration of the map to do just that.

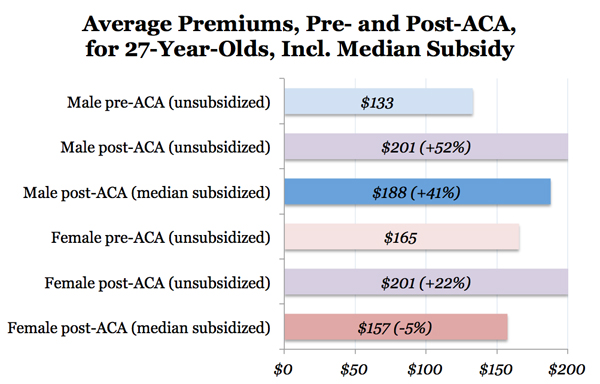

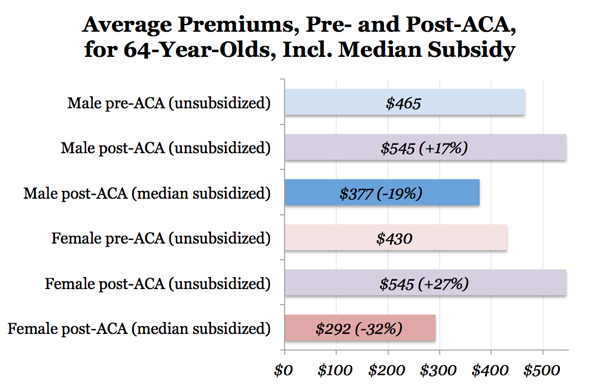

Today’s release, with the third iteration of the map, contains both premium and subsidy data for every state except Hawaii. (Believe it or not, we’ve had success mining data from every exchange website but Hawaii’s.) This nearly-complete analysis finds that the average state will face underlying premium increases of 41 percent. Men will face the steepest increases: 77, 37, and 47 percent for 27-year-olds, 40-year-olds, and 64-year-olds, respectively. Women will also face increases, but to a lesser degree: 18%, 28%, and 37% for 27-, 40-, and 64-year-olds.

Biggest winners: NY, CO, OH, MA; Biggest losers: NV, NM, AR, NC

Eight states will enjoy average premium reductions under Obamacare: New York (-40%), Colorado (-22%), Ohio (-21%), Massachusetts (-20%), New Jersey (-19%), New Hampshire (-18%), Rhode Island (-10%), and Indiana (-3%). Most, but not all, of these states had heavily-regulated individual insurance markets prior to Obamacare, and will therefore benefit from Obamacare’s subsidies, and especially its requirement that everyone purchase health insurance or pay a fine.

The eight states that will face the biggest increases in underlying premiums are largely southern and western states: Nevada (+179%), New Mexico (+142%), Arkansas (+138%), North Carolina (+136%), Vermont (+117%), Georgia (+92%), South Dakota (+77%), and Nebraska (+74%).

If you’re interested in more details about our methodology, you can find them here. As with our past work, we calculated an average of the five least-expensive plans in every county in a state pre-Obamacare, adjusted to take into account those with pre-existing conditions and other health problems. We then did the same calculation with the five least-expensive plans in every county in the Obamacare exchanges. We then used these county-based numbers to come up with a population-weighted state average pre- and post-Obamacare.

Exchange plans narrow your choice of doctor, despite higher costs

The key thing to understand about our before-and-after comparison is that it is an average. If you’re healthy today, you will face steeper rate increases than these figures indicate. If you have a serious medical condition, however, and haven’t been able to find affordable health coverage as a result, you will do much better under Obamacare than the average person. Men will face steeper increases than women in most states, because women consume more health care than men do, and Obamacare forbids insurers to charge different prices on the basis of gender.

In addition, our comparison ignores other differences between pre-Obamacare and post-Obamacare plans. For example, in some cases, people looking for comparably-priced coverage on the exchanges will need to accept higher deductibles and other cost-sharing arrangements.

Importantly, post-Obamacare exchange plans will typically have narrow networks of physicians and hospitals, especially excluding those tied to prestigious medical schools. In today’s Wall Street Journal, Edie Sundby, who struggles with gallbladder cancer, argues that her pre-Obamacare access to leading academic cancer centers like Stanford has “kept me alive,” and notes that the plans available to her on the exchange don’t allow her to keep her doctor.

Elderly will receive massive subsidies, thanks to younger people

Thanks to community rating, a key feature of Obamacare, insurers are only allowed to charge their oldest customers three times the amount they charge their youngest customers. Because 64-year-olds consume on average six times as much health care as 19-year-olds, this rule has the effect of driving up the cost of insurance for young people.

But there’s a double whammy. Because premiums for those nearing retirement can still be three times higher than those of younger Americans, elderly individuals will disproportionately benefit from Obamacare’s subsidies. The subsidies increase in proportion to the percentage of your income that is tied up in health insurance; for elderly people whose premiums are much higher, the subsidies are higher too.

And when I say young people, I particularly mean young men. A young woman of average income in the average state will experience little net change in premium costs, if you take subsidies into account; 40-year-old women will see an average increase of 9 percent, and 27-year-old women will see an average decrease of 5 percent. (However, as I noted above, women in good health will see meaningfully higher increases than these averages reflect.)

Let’s take the two extremes. If you’re a 27-year-old man, your average premium under our methodology, pre-Obamacare, is $133 a month. Post-Obamacare, that increases to $201. If you add in the subsidies that accrue to someone with the median income of a 27-year-old man, the net cost of Obamacare insurance goes down slightly to $188. That’s a 41 percent increase, despite the impact of subsidies.

If you’re a 64-year-old woman, on the other hand, your average pre-Obamacare premium was $430 a month. Post-Obamacare, the underlying premium increases to $545 a month. But when you factor in subsidies for the average 64-year-old woman, the net cost of Obamacare insurance drops to $292. That’s a 32 percent decrease, inclusive of subsidies, from pre-Obamacare premiums, and a 46 percent discount off of post-Obamacare prices.

The irony is that, in 2012, younger voters overwhelmingly supported President Obama, while older voters backed Mitt Romney. Obamacare, in the average state, is a massive transfer of wealth from the young to the old.

This all assumes, of course, that the exchanges eventually work

Right now, the headlines are dominated with stories about the deep and thorough dysfunction of the federally-built Obamacare insurance exchange. It’s a serious problem. If the exchanges aren’t fixed soon, the likely outcome is that older, sicker, and poorer people sign up, while everyone else goes without coverage. That, in turn, will imbalance the insurance pool in the exchanges, making its products more expensive and subsidy-dependent. Those facing cancellation of their existing coverage face the greatest risk under the worst-case scenario.

But there is a best-case scenario, especially from the standpoint of the law’s supporters. It’s that the exchanges eventually get fixed, and turn out to be popular, even among the young men—the “bros”—who bear the steepest costs under the new system. If they do, not only will Obamacare be here to stay, but the law could end up evolving into an effective replacement for our older, single-payer health-care entitlements, Medicare and Medicaid.

From where we stand today, unfortunately, there is no reason to believe that the Obama administration has a handle on the problems with the federal exchange. Young men seem no more likely to buy a costlier insurance product than they were to buy one, pre-Obamacare, that was more affordable. And so we should remain concerned about the likelihood of the law’s ultimate success.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2014-08-20 11:26:132015-10-08 00:00:0049-State Analysis: Obamacare To Increase Individual-Market Premiums By Average of 41 Percent

The Best of MichBusiness awards program is dedicated to one thing – recognizing those companies and individuals that make Michigan a top-notch place to do business.

The Best of MichBusiness event celebrates success in grand style, as the most exciting and connected business awards and networking opportunity in the State of Michigan. We expect approximately 100 honorees in various categories and over 300 attendees from all walks of life, representing all types of businesses in Michigan.

The MichBusiness Awards is the place to be this November to connect with the best in the state. Mark your calendar for November 18th, 2014. We will see you at the International Banquet Center at 5:30!

Nomination Categories Include: Designing Stars, Education Excellence, Health Care Visionaries, HR Wizards & Partners, Manufacturing Inspirations, Marketing Savants, Media Marvels, Non-Profit Beacons, One Person Wonder, Sales Monsters, Stellar Start Ups, Technology Gurus, The Best of Hatched™, The CEO of CEOs, MichBusiness Champion of the Year, and Lifetime Achievement Awards

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2014-08-12 16:00:502015-10-08 00:00:00Nomination Deadline Approaching – The Best of MichBusiness!

Step 1: Form a committee.

Step 2: Over-think it.

Step 3: Make sure you please everybody.

Looking for a sure-fire way to take all of the creativity, panache, impact and stickiness out of your brand? Creativity is nothing a committee can’t fix! Allow us to demonstrate, using one of modernity’s most memorable and recognizable taglines:

Comment: “The tagline MUST be accompanied by the logo at all times. Please correct and resubmit.”

Comment: “Better, but now it’s too small. Why did you crop it? Anyway, how will anyone know what company this is for? Please include our legally approved corporate name. Don’t forget Registration marks.”

Comment: “Now we’re getting there. Do we need the trademark under the tagline as well?” “In fact, let’s take this conversation offline…”

Time to Second-Guess the Strategy

“…There. Just wanted to share a few other concerns. I’m worried that “Just do IT” is overly suggestive. We need to be sensitive and consider all stakeholders. We are a sports brand. Shouldn’t we be specific? Please share some additional taglines before we send to Creative for design treatments.”

JUST DO SPORTS

JUST DO ATHLETICS

JUST WIN, BABY (AT SPORTS OR ATHLETICS)

JUST EXCEL.

JUST EXCEL! (exclamation point for added emphasis)

Comment: “I think all of these are steps in the right direction, but I don’t think any of them capture the fashion-forward ethos of our heritage. We need to convey both that we are an athletic apparel company and that we are a premier fashion-oriented retail player. Please revise and resubmit. Also consider our leadership position in the category.”

MANAGING YOUR SUCCESS ON THE ATHLETIC FIELD OF PLAY, ONE SPORTING CONTEST AT A TIME.

ELITE PROVIDER OF SPORTS APPAREL AND FASHION-CENTRIC COMPETITIVE GEAR.

Comment: “Great builds! But you’re leaving out our competitive spirit. If you can infuse some of that, I think we’re there. Great work!”

MANAGING YOUR SUCCESS ON THE ATHLETIC FIELD OF PLAY, ONE SPORTING CONTEST AT A TIME…FOR THE WIN!

ELITE PROVIDER OF WINNING SPORTS APPAREL AND FASHION-CENTRIC COMPETITIVE GEAR GENERATING AMAZING OUTCOMES.

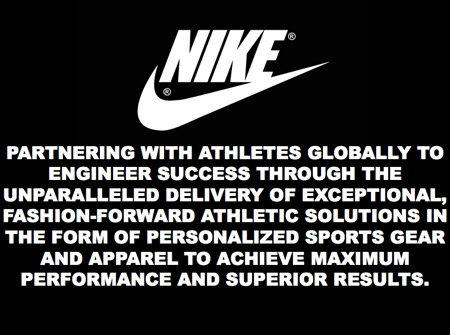

ENGINEERING SUCCESS THROUGH THE UNPARALLELED DELIVERY OF EXCEPTIONAL, FASHION-FORWARD ATHLETIC GEAR AND APPAREL TO ACHIEVE MAXIMUM PERFORMANCE.

Comment: “Love the new idea! Let’s run with that. Tim voiced a valid concern that we’re not promoting the fact that we’re a global organization. And Susan made the excellent point that we’re really in the business of forming partnerships with our customers. We sell solutions, not clothes. I’m faxing you a few additional redlines. Final tweaks, then let’s get this off to Creative to really make it sing, and have HR and Legal give their blessing and finalize.”

Finished Product:

Comment: “Perfect! Now…what’s our go-to-market strategy? I’ll form a committee and get on everyone’s calendar…”

Moral of the story: Less is more…you know that. Just do it.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2014-08-12 16:00:452015-10-08 00:00:00How To Suck The Cool Out of a Campaign

By Mike Semanco

President & COO, Hitachi Business Finance

“Failure is not an option!” Really???

How many successful companies have used this line as a way to motivate its employees, to increase sales, become more efficient, improve client service and develop a culture they are proud of? Not one!

As a parent of three teenage children, I would never tell my kids that failure is not an option. I always want them to try new things. That is how kids learn. Mistakes are made, they learn, adjust and go on. How much fun is it spending all your time perfecting your baseball swing and never getting a chance to bat? Kids have a natural tendency to try anything. They don’t have a fear of failing. They scrape their knee and hop back on the skateboard to try the trick again until they get it right. As a parent, you are always concerned but it usually works out in the end.

Most entrepreneurs think the same way. They come up with an idea, do some initial market testing with friends and family, and are ready to launch. They have no fear of failing because if that idea doesn’t get the results they want, they try something else. If that doesn’t work, they pivot, and try again and again until they get it right. That is what makes creating a business or product so enjoyable.

Why is it that some companies create a culture where failure is not an option? Did they start out this way or did they evolve into a stodgy organization? Some companies have success in spite of themselves, but I am sure there was a point in the company’s lifecycle when failure was an option. My guess is that those risk takers left to start other ventures.

In today’s ever changing business world, you have to take risks, albeit as calculated as possible. Failure is an option. That is how companies evolve, employees learn and develop, and great cultures get created. Many of us spend the majority of our waking hours working – why should we do it in fear of making a mistake? Managers and executives should reward employees for trying new ideas and taking calculated risks. At some point in that manager or executive’s career, they took risks and can tell stories of failures they had along the way. Most can then tell you what they did different the second time around. It’s called experience. Why not give your employees the same opportunity and create an environment where failure is an option. It is much more rewarding.

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2014-08-12 16:00:402015-10-08 00:00:00Failure Is Not An Option?

You’ve spent a lot of time, effort and money trying to communicate the right message to your prospects.

Now if they would just stop doing what they do and pay attention to you, your offer and your brilliant marketing then you could help them to improve their condition, right? Well listen up and…

Put the Remote Control Down!

How do you break through preoccupation and get your prospect’s attention? My daughter stands in front of the TV and says, “Dad turn off the TV and put the remote control down!”

That works for her. However, you may want to answer these starter questions to reveal marketing clues about your prospects.

ONE What methods do you use in your promotions, advertising and brochures to effectively interrupt the preoccupied prospect? How do you consistently get your targets attention? Is it working? How do you know for sure?

Hint: Your marketing should contain powerful “hot-button” related headlines. They should tie to benefits or problems your product or service provides.

TWO Once interrupted, what methods have you developed to keep your prospect engaged sufficiently long enough that you can begin to educate them on the value of your product/service?

Hint: People don’t want to be sold as much as they would like to buy based on an educated decision. If they are not ready to buy today then find a way to educate them now and over time.

THREE What’s your offer? Is it articulated in a way that’s low risk upfront and provides an opportunity to build trust? Or, is it a buy it all now or nothing proposition?

Hint: This article for the MBPA is a no-risk educational offer. It’s designed to create real informational value and provide some insight into what the MBPA can offer to help you grow your business.

FOUR Are your promotional materials designed to primarily get the sale now? This is also known as “cherry picking” the low hanging fruit. Or are your materials intended to get the prospect on an educational spectrum where you then systematically follow up and educate them with a targeted message over time? One day your prospect will be ready. If you follow up correctly, build trust, offer real value, then likely you’ll get the call.

Hint: Marketing is like dating. You build trust gradually until you’ve earned the right to go to the next step.

Daron Powers consults and speaks with professionals, small, midsized and fortune 500 companies and collaborates with businesses to develop and refine marketing strategy/plans, content for websites, article writing, online videos, web marketing, sales presentations, selling tools, etc. Visit his two websites: DaronPowers.com and OnlineVideoPower.com. Email: info@OnlineVideoPower.com. Phone: 248-470-8379

https://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.png00michbusinesshttps://michbusiness.com/wp-content/uploads/2023/08/MichBusiness_logo_horizontal.pngmichbusiness2014-08-12 16:00:352015-10-08 00:00:00Four Ways to Break Your Prospect’s Preoccupation Barrier and Be Seen & Heard

By Larry Grudzien

By Larry Grudzien By Avik Roy

By Avik Roy

The Best of MichBusiness awards program is dedicated to one thing – recognizing those companies and individuals that make Michigan a top-notch place to do business.

The Best of MichBusiness awards program is dedicated to one thing – recognizing those companies and individuals that make Michigan a top-notch place to do business.

By Mike Semanco

By Mike Semanco By Daron Powers

By Daron Powers